Mzdy v komerční sféře se příští rok zvýší v průměru o 4,5 procenta, více než šest procent chce přidat sedmina firem. Vyplývá to z analýzy Comp&Ben Asociace, která sdružuje na českém trhu klíčové zaměstnavatele a zabývá se analýzou mezd a systémy odměňování. Nejvíc si podle ní polepší technické provozní pozice a specialisté, zatímco top management zaznamená nejnižší nárůsty. Nejvyšší zvýšení se očekává v sektorech výroby, technologií a služeb, naopak nižší ve financích nebo IT.

Medián nárůstu dosáhne podle analýzy pěti procent. V roce 2025 by se měl vrátit růst reálných mezd, i když tempo zvyšování mírně zpomalí. Hodnoty mezd, s nimiž Comp&Ben Asociace v analýze pracuje, vycházejí z tržního průzkumu mezi firmami z komerčního sektoru z říjnu a listopadu 2024. Průměrná hrubá mzda v Česku stoupla v letošním třetím čtvrtletí meziročně o sedm procent na 45.412 korun. Při zohlednění inflace, která činila 2,3 procenta, mzda reálně vzrostla o 4,6 procenta.

Růst mezd ve výrobních společnostech je vyšší než narůst výdělků v nevýrobních společnostech. „Nejvíce si polepší technické provozní pozice s růstem o 4,7 procenta a specialisté se 4,6 procenta, kterých je na trhu nedostatek. Nejméně dostane přidáno top management, a to o 4,1 procenta. Dynamika mzdového trhu se začíná pomalu stabilizovat a neočekáváme rychlejší tempo růstu. Jedinou výjimkou mohou být některé specializované pozice,“ uvedl ředitel Comp&Ben Asociace Tomáš Jurčík.

Vyšší nárůsty se budou podle něj týkat zejména specializovaných technických pozic a vybraných IT odborníků, kteří jsou důležití pro digitalizaci a zavádění nových technologií. Jejich dlouhodobý nedostatek jim zajišťuje výrazně lepší vyjednávací pozici.

V prvních čtyřech měsících plánuje zvýšení mezd podle analýzy 76 procent zaměstnavatelů v komerčním sektoru. Zaměstnanci se nejčastěji dočkají zvýšení mzdy v lednu a v dubnu. Nejvíce, v průměru o téměř pět procent, budou přidávat firmy v sektoru výroby, technologie a rychloobrátkového zboží. Naopak nejméně, kolem čtyř procent, v sektoru finančním a informačních technologiích.

Lze očekávat, že odbory budou mít v některých sektorech tendenci vyvíjet tlak na vyšší nárůsty mezd, uvedli autoři analýzy. Odbory se podílejí na vyjednávání o konečné výši nárůstů mezd pro příští rok v téměř 40 procentech firem zapojených do průzkumu. Zaměstnavatelé však podle jeho výsledků budou ochotni navyšovat pouze v sektorech, kde to ekonomická realita umožní.

Comp&Ben Asociace sdružuje na trhu v Česku klíčové zaměstnavatele a zabývá se analýzou mezd a systémy odměňování v soukromém sektoru. Asociace vznikla ve spolupráci s Vysokou školou ekonomickou v Praze. Mezi zakládající členy patří řada významných zaměstnavatelů, například skupina PPF, Vodafone, Foxconn, Zentiva, PwC ČR, Siko, Makro, Notino, ČEZ, T-Mobile, Raiffeisen Bank, Hornbach, Mattoni, Aterra Group, Mercer, Miele, PM-tech či Orlen Unipetrol.

Meziroční inflace zůstala v listopadu na 2,8%, analytici čekali růst

Spotřebitelské ceny v Česku v listopadu meziročně vzrostly o 2,8 procenta, stejně jako v říjnu. Dražší bylo bydlení, lihoviny či tabákové výrobky. Meziměsíčně byly ceny vyšší o 0,1 procenta. Údaje dnes zveřejnil Český statistický úřad (ČSÚ). Analytici očekávali, že inflace v meziročním vyjádření zrychlila na tři procenta. Listopadová inflace byla pod očekáváním, pomaleji zdražovalo víc oddílů, upozorňují analytici, které oslovila ČTK.

„V listopadu ceny oproti loňskému roku vzrostly stejně jako v říjnu o 2,8 procenta. Vývoj cen v jednotlivých oddílech spotřebního koše byl však odlišný. Jediným oddílem, kde ceny meziročně klesly, byl oddíl odívání a obuv, a to o necelé jedno procento,“ uvedla vedoucí oddělení statistiky spotřebitelských cen ČSÚ Pavla Šedivá.

Ke zrychlení meziročního cenového růstu došlo v listopadu zejména u potravin a nealkoholických nápojů. Ceny výrobků ve skupině mléko, sýry, vejce přešly z říjnového poklesu o 0,1 procenta v růst o 4,3 procenta. Ceny vajec dokonce přešly z poklesu o 5,6 procenta v říjnu v listopadový nárůst o 31,7 procenta. Ceny masa klesly o 1,3 procenta.

Zpomalení růstu cen statistici zaznamenali u elektřiny, která v listopadu sice zdražila o 9,2 procenta, v říjnu to však bylo o 10,5 procenta. Pokles cen zemního plynu v listopadu zrychlil na 2,9 procenta z 2,3 procenta v předchozím měsíci. Pohonné hmoty a oleje zlevnily meziročně o 7,6 procenta, zatímco v říjnu pokles činil 11,4 procenta.

Na meziroční růst cenové hladiny v ČR měly v listopadu nadále největší vliv ceny bydlení. Ceny nájemného z bytu byly vyšší o 6,3 procenta, vodné zdražilo skoro o 11 procent a stočné o 13,4 procenta. Za teplo a teplou vodu lidé platili o 8,5 procenta více.

Další v pořadí vlivu byly ceny v oddíle alkoholické nápoje, tabák. Lihoviny meziročně zdražily o 3,3 procenta, pivo o tři procenta a tabákové výrobky o sedm procent. Stravovací služby podražily o 6,7 procenta a ubytovací služby o 8,8 procenta. Ceny dovolených s komplexními službami se zvýšily o 6,6 procenta.

Na meziroční snižování celkové cenové hladiny působily v listopadu ceny v oddíle odívání a obuv. Oblečení zlevnilo o půl procenta a obuv zlevnila o 2,3 procenta.

Ceny zboží v listopadu úhrnem vzrostly o 1,4 procenta. Služby meziročně zdražily o 5,2 procenta.

Statistici dnes zveřejnili také informace o říjnovém vývoji cen v zahraničním obchodu. Oproti září se ceny vývozu zvýšily o 0,9 procenta a ceny dovozu stouply o procento. „V říjnu byly ceny vývozu a dovozu značně ovlivněny vývojem kurzu koruny vůči euru a dolaru,“ podotklvedoucí oddělení statistiky cen průmyslu a zahraničního obchodu ČSÚ Vladimír Klimeš. V meziročním porovnání vzrostly vývozníceny o tři procenta a dovozní ceny o 0,6 procenta, významně se podle statistiků snížily ceny pohonných hmot.

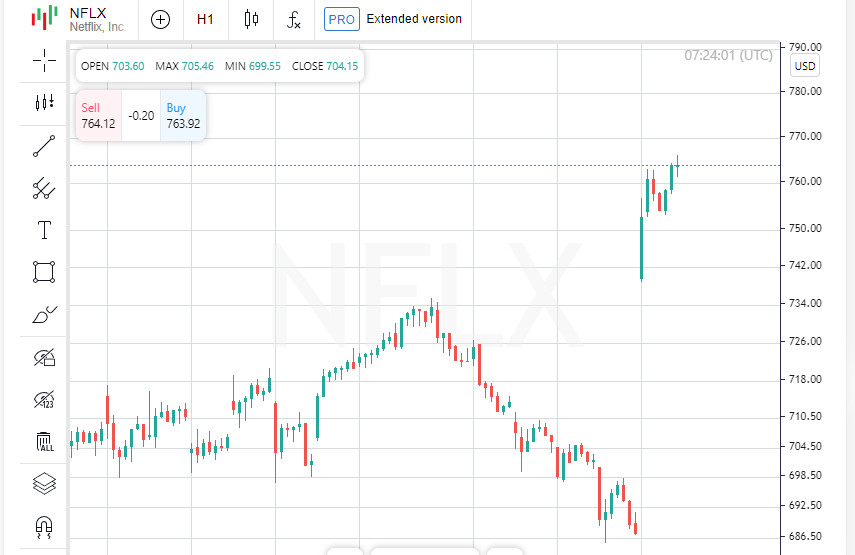

Netflix's rise boosted the communications sector, which rose 0.9% to lead the 11 S&P 500 sectors. Meanwhile, the information technology sector added 0.5%, also helping to strengthen the overall market.

The major U.S. stock market indices continued to rise on Friday. The S&P 500 rose 23.20 points, or 0.40%, to close at 5,864.67. The Nasdaq Composite added 115.94 points, or 0.63%, to close at 18,489.55. The Dow Jones Industrial Average rose 36.86 points, or 0.09%, to close at 43,275.91. Dow Jones Gains Subdued

The Dow posted its fifth record close in the last six sessions. However, its gains were less dramatic due to a decline in American Express shares. The financial giant lost 3.1% after reporting quarterly earnings that missed analysts' expectations.

Despite the disappointment from American Express, the financial sector as a whole ended the earnings season on a positive note. However, the S&P Banks Index, which measures banking stocks, fell 0.1%, snapping a five-week winning streak.

Positive financial reports and favorable economic indicators helped propel the indices steadily higher. However, it's worth noting that the S&P 500 trades at 22 times projected earnings. This, coupled with expectations for strong corporate results and uncertainty surrounding the upcoming US presidential election on November 5, could lead to increased volatility and market corrections.

Investors have shown increasing interest in small-cap stocks in recent days. Over the week, the Russell 2000 and S&P Small Cap 600 indexes outperformed the major indices. However, both indexes fell on Friday, demonstrating a weakening interest in small companies amid overall market optimism.

Amid weaker oil prices, the energy sector was the only one in the S&P 500 to show negative dynamics, falling 0.4%. The sector was particularly pressured by shares of SLB, which fell 4.7% after the publication of quarterly results that did not meet investor expectations. The decline also weighed on other oilfield services players such as Baker Hughes and Halliburton, which fell 1.3% and 2.1%, respectively.

The energy sector was the weakest performer this week, falling 2.6%. One of the reasons was a significant 7% drop in U.S. oil prices, caused by concerns about slowing demand from China and uncertainty caused by the ongoing conflict in the Middle East.

CVS Health fell 5.2% after the company announced a CEO change. Karen Lynch was replaced by David Joyner, a CVS veteran who took over the CEO's chair. In addition to the management change, CVS withdrew its 2024 profit guidance, which also weighed on the stock.

The news of the CVS management change affected not only the company itself, but also other health insurers. For example, shares of Cigna and Elevance Health also declined, with the latter closing down 3.1%, reaching its lowest level in 15 months.

Trading volume on U.S. exchanges amounted to 10.62 billion shares, slightly below the average of 11.56 billion shares over the past 20 sessions. Investors will be keeping a close eye on semiconductor stocks in the coming weeks. Conflicting reports from overseas leaders in the sector have led to some volatile trading sessions, putting the semiconductor industry in the spotlight.

As the foundation for many modern technologies, semiconductors remain the center of attention for investors and analysts alike. Companies that manufacture chips and the equipment to create them closely monitor global economic developments, and their stocks often act as an indicator of overall market sentiment.

The Philadelphia SE Semiconductor Index (SOX) posted a strong gain of more than 40% in the first half of the year, although its momentum has slowed a bit recently. To date, the index is still up about 25% for 2024, outpacing the 22.5% gain of the benchmark S&P 500.

The semiconductor and related equipment sector is a significant part of the S&P 500, accounting for about 11.5%. Nvidia is particularly eye-catching, with its market capitalization almost equal to Apple's, accounting for 6.8% of the index's weight.

The chip sector has seen wild swings in the past week. Semiconductor-related stocks fell on Tuesday after a disappointing forecast from ASML, Europe's largest technology company. ASML warned of a decline in sales and orders in 2025, prompting a sharp market reaction.

However, investors breathed a sigh of relief on Thursday when Taiwan Semiconductor Manufacturing Co, a leading maker of AI chips, reported a stunning 54% jump in quarterly profit, well above expectations.

Despite the mixed news, the SOX index ended the week down 2.5%, while the S&P 500 managed to post a small gain of 0.5%, highlighting the different dynamics of different sectors.

In the coming week, the semiconductor sector will be closely watching the earnings reports of key players. Among them are Texas Instruments and equipment maker Lam Research, whose results could set the direction for the market going forward.

Texas Instruments products are used in a variety of industries, from automotive to industrial, making the company a bellwether for industries where demand for chips remains weak. Daniel Morgan, portfolio manager at Synovus Trust, notes that the company's report could provide an answer to the question of whether these sectors are starting to recover.

Morgan also emphasized that the semiconductor sector as a whole trades at a price-to-book ratio of 5.6x, which he believes is a reasonable number. By comparison, the 2021 P/B ratio was over 8x, indicating that the market was overheated at the time.

Next week's Advanced Micro Devices (AMD) earnings report will be an important marker for demand for AI-related chips. The report will provide a preview of Nvidia's expected results next month. If AMD shows strong 2025 guidance for its AI chips, it will be a positive signal for the entire sector, analyst Meili said.

Next week's semiconductor earnings are set to come as part of a busy corporate season in the U.S. Among the more than 100 S&P 500 companies reporting results will be giants such as Tesla, Coca-Cola and IBM.

Chuck Carlson, CEO of Horizon Investment Services, undercores the importance of the semiconductor industry to the overall market. The sector accounts for a significant portion of market cap, making its performance a determining factor in the overall health of the financial market.

БЫСТРЫЕ ССЫЛКИ

Контакты

Контакты