Tuesday's trading session on U.S. stock markets closed without significant movements, although Nasdaq showed a slight rise. Investors continue to closely monitor the dynamics of Treasury bond yields while awaiting corporate earnings reports to better assess the state of the U.S. economy.

"In recent days, the market has been trying to digest changes in Treasury bond yields. We're seeing quite significant fluctuations in this segment," said Jack Janasiewicz, portfolio manager at Natixis Investment Managers Solutions.

During volatile trading, the Dow Jones Industrial Average (.DJI) fell by 6.71 points, or 0.02%, to 42,924.89. The S&P 500 (.SPX) dropped by 2.78 points, or 0.05%, closing at 5,851.20. Meanwhile, Nasdaq Composite (.IXIC) saw a gain of 33.12 points, or 0.18%, reaching 18,573.13.

Nearly half of the S&P sectors closed in positive territory, with the consumer goods sector (.SPLRCS) leading the charge, up by 0.92%, driving market optimism.

Earlier in the day, the yield on 10-year Treasury bonds hit 4.222%, its highest level since July 26, as investors reassessed expectations for the Federal Reserve's monetary policy. However, yields dipped slightly during the session.

"The main concern is rising interest rates and fears that the Federal Reserve may have been too aggressive in September. This is fueling a global sell-off in bonds," noted Michael Green, portfolio manager at Simplify Asset Management.

Shares of GE Aerospace (GE.N) tumbled by 9%, despite an optimistic profit forecast for 2024. Persistent supply chain issues negatively impacted the company's revenue, weighing down the broader industrial index (.SPLRCI), which fell by 1.19%.

At the same time, the technology sector (.SPLRCT) posted a modest gain of 0.15%. Leading the charge was Microsoft (MSFT.O), with its shares rising by 2.08%, maintaining a sense of optimism amid market instability.

"Earnings season is traditionally accompanied by high volatility, especially given the uncertainty surrounding future interest rate changes," explained Chuck Carlson, CEO of Horizon Investment Services.

Experts expect the next few weeks to remain turbulent for stock markets, as investors closely watch corporate earnings, economic data, and the outcome of U.S. elections, followed by the Federal Reserve's decision.

According to CME's FedWatch data, traders are pricing in an 89.6% probability of a 25 basis point rate cut in November. This indicates strong market confidence in a dovish stance from the Federal Reserve.

Verizon (VZ.N) fell by 5.03% after its third-quarter financial results failed to meet market expectations. The telecom giant underperformed revenue forecasts, leading to a negative reaction from investors.

Shares of 3M (MMM.N) declined by 2.31%, despite the company raising its full-year adjusted profit forecast. The market seemed unimpressed, responding with a sell-off.

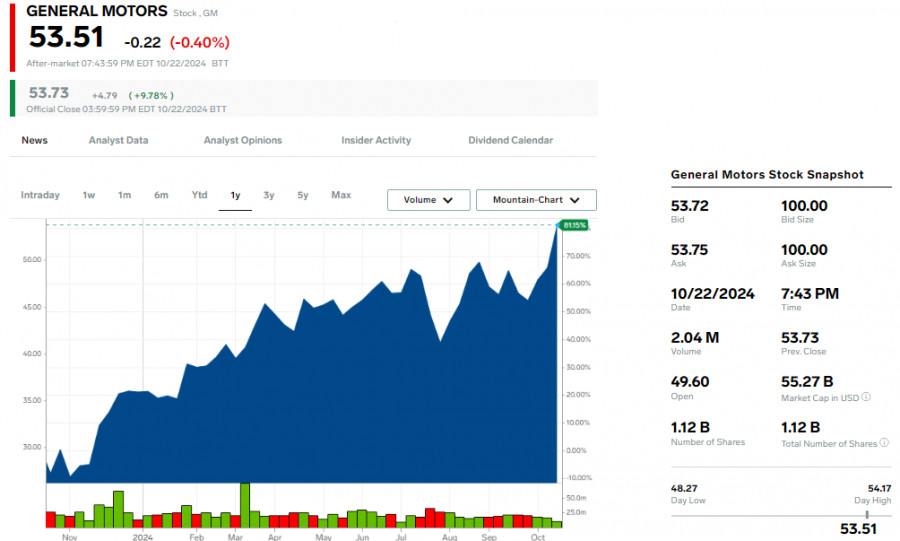

Amid the broader market tension, General Motors (GM.N) surged by 9.81% after its third-quarter results exceeded Wall Street's expectations. In contrast, Lockheed Martin (LMT.N) dropped by 6.12% following the release of its earnings, which failed to impress analysts.

Stocks of companies sensitive to interest rates, particularly in the housing sector, took a hit during the latest trading session. The PHLX Housing Index (.HGX) dropped by 3.05%, driven largely by a 7.24% decline in PulteGroup (PHM.N) shares, despite the company surpassing earnings and revenue forecasts.

"While the earnings themselves were quite solid, companies highly exposed to interest rate changes are likely facing some headwinds, as investors grapple with the overall interest rate narrative," said Carlson.

Investor attention is now turning to Baker Hughes (BKR.O) and Texas Instruments (TXN.O), which are set to report earnings after the market closes. Market participants are eagerly awaiting these figures to gauge the broader corporate landscape.

On the New York Stock Exchange (NYSE), decliners outnumbered gainers by a ratio of 1.37 to 1. Additionally, 186 new highs and 58 new lows were recorded during the trading session.

The S&P 500 saw 15 new 52-week highs and 4 new lows, while the Nasdaq Composite registered 72 new highs and 61 new lows. Total trading volume on U.S. exchanges reached 11.45 billion shares, surpassing the 20-day average of 11.28 billion.

Gold prices reached a record high of $2,750.9 per ounce on Wednesday, driven by ongoing Middle East tensions and uncertainty surrounding the Federal Reserve's future moves and the U.S. election. Meanwhile, the dollar strengthened, putting pressure on both the yen and euro, while Asian stocks saw slight gains as investors remained cautious ahead of the contested U.S. elections.

The broad MSCI index of Asia-Pacific shares outside Japan (.MIAPJ0000PUS) climbed 0.3% in recent trading. Meanwhile, Japan's Nikkei (.N225) fell 1% ahead of the upcoming national elections this weekend.

Chinese and Hong Kong stocks finished higher on Wednesday, buoyed by government promises to support the economy. However, the specifics of the timing and scale of the stimulus measures remain unclear, keeping investor optimism in check.

In Europe, the mood remained subdued: Eurostoxx 50 futures edged up 0.08%, while Germany's DAX futures rose by 0.11%. However, FTSE futures dipped slightly, falling by 0.04%, reflecting continued caution among European traders.

Investors are also paying close attention to the prospect of Donald Trump's potential return to the White House. His policies, which include tariffs and stricter controls on illegal immigration, are expected to drive inflation higher. This has further strengthened the dollar as markets anticipate U.S. interest rates remaining higher for longer than previously expected.

The odds of Trump defeating Democratic candidate and Vice President Kamala Harris have improved on betting platforms. However, polls show that the presidential race remains highly competitive and too close to call.

With less than two weeks to go before the November 5 election, investors are bracing for increased market volatility. The yield on 10-year U.S. Treasury bonds hit 4.234% during Asian trading hours, the highest level in three months, reflecting expectations of prolonged high rates.

The sell-off in U.S. Treasury bonds has accelerated this week as markets recognize the risk that the Federal Reserve could reignite inflation if it eases its stance in an improving economy. Prashant Newnaha, senior Asia-Pacific rates strategist at TD Securities, highlighted the growing concerns about inflation.

The improved odds of Donald Trump winning the upcoming U.S. election have also dampened market expectations of further Fed easing in 2025. There's a chance that the Federal Reserve may take a back seat for six months next year, which could alter the trajectory of monetary policy.

Expectations of slower Fed rate cuts have pushed the dollar higher in recent weeks. The dollar index, which measures the currency's value against six major rivals, climbed to 104.17, its highest since August 2.

The yen fell to a three-month low of 152.28 against the dollar, while the euro dropped to $1.0792, its lowest since August 2. Both currencies are facing headwinds as the dollar continues to strengthen.

Gold prices soared to a new record high of $2,750.9 per ounce, as the ongoing conflict in the Middle East and uncertainty surrounding the Fed's future moves and the U.S. election drive demand for safe-haven assets.

Oil prices saw a slight correction after sharp gains earlier in the week. Brent crude futures fell 0.14% to $75.93 per barrel, while West Texas Intermediate (WTI) crude futures dropped 0.18% to $71.61 per barrel.

SZYBKIE LINKI

Skontaktuj się z ForexMart

Skontaktuj się z ForexMart